Advertisement

)

AT A GLANCE

- Concept: Forward Settlement: Traders agree on parameters today but deliver the actual physical assets weeks later.

- Concept: Asset Fungibility: Standardized rules mathematically treat unique residential mortgages as perfectly interchangeable financial instruments.

- Concept: Cheapest-to-Deliver: Sellers supply the lowest-quality qualifying mortgage pools to maximize their financial profit.

- Concept: Rate Locking: Selling future mortgages allows lenders to guarantee fixed interest rates to prospective homebuyers instantly.

HOW IT WORKS

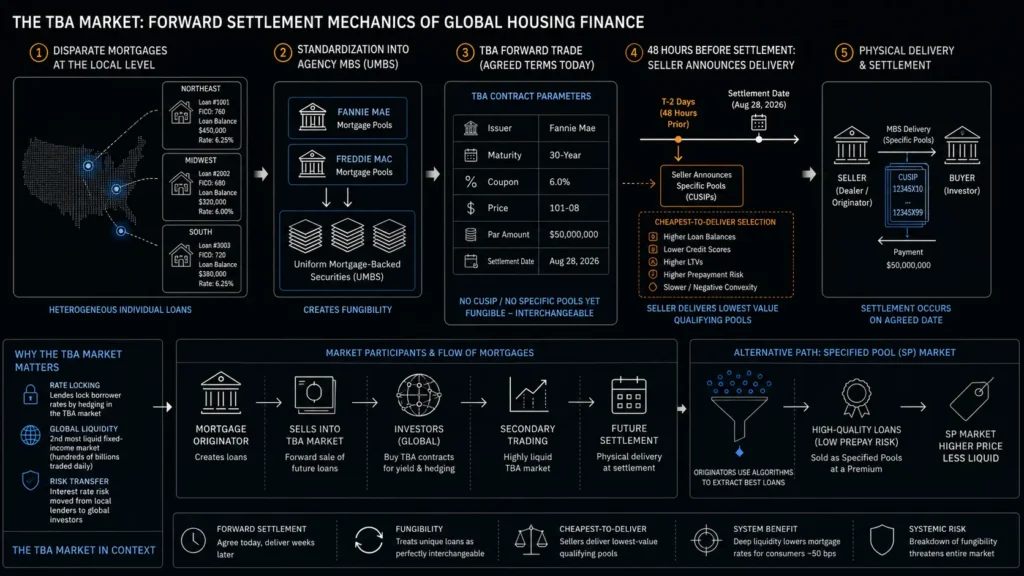

US residential mortgages are inherently chaotic. Every home loan features a different borrower credit score, geographic location, and underlying property value. If global investors had to analyze every single local mortgage before buying it, the transaction costs would paralyze the housing market.

To solve this friction, government-sponsored enterprises like Fannie Mae and Freddie Mac bundle these individual loans into standardized Mortgage-Backed Securities (MBS). However, the true liquidity engine of this system is the To-Be-Announced (TBA) forward market. Operating under strict parameters set by the Securities Industry and Financial Markets Association (SIFMA), the TBA market allows financial institutions to trade these securities without knowing exactly which mortgages they are buying.

In a TBA trade, the buyer and seller agree on only six basic parameters: issuer, maturity, coupon rate, price, par amount, and settlement date. They do not specify the actual CUSIP identifier of the mortgage pool at the time of the trade. The market operates on the absolute economic assumption of fungibility—that any MBS pool meeting these basic six criteria is perfectly interchangeable with any other.

Exactly forty-eight hours before the predetermined monthly settlement date, the seller finally “announces” which specific mortgage pools they will deliver to the buyer to fulfill the contract. Because the seller controls this physical delivery, they execute a “cheapest-to-deliver” strategy. They mathematically select the mortgage pools with the least desirable prepayment characteristics—meaning the loans most likely to be paid off early or refinanced—and deliver those to the buyer.

WHY IT MATTERS NOW

The TBA market trades hundreds of billions of dollars every single day, making it the second most liquid fixed-income market in the world, trailing only US Treasury bonds. This extreme liquidity represents the absolute bedrock of American housing affordability.

When a consumer walks into a bank to secure a thirty-year fixed-rate mortgage, the bank immediately sells that loan into the TBA forward market. Because the TBA trade settles weeks in the future, the bank essentially sells a mortgage that does not technically exist yet. This forward-selling mechanic completely offloads the interest rate risk from the local bank to the global capital markets, allowing the lender to lock in the consumer’s mortgage rate instantly.

If this forward market did not exist, local banks would have to hold mortgages on their own balance sheets, requiring massive capital reserves to survive interest rate fluctuations. They would pass those warehousing costs directly to the consumer, drastically increasing the baseline cost of homeownership. The sheer volume and velocity of TBA trading narrow the bid-ask spreads so tightly that they actively subsidize consumer borrowing costs by roughly half a percentage point.

Today, as the Federal Reserve navigates quantitative tightening, the TBA market faces severe structural stress. The central bank is no longer acting as the guaranteed buyer of last resort for these securities. Private money managers, real estate investment trusts, and foreign central banks must absorb this massive daily supply of mortgage debt, forcing the cheapest-to-deliver pricing mechanics to dynamically recalculate the true cost of global capital.

WHAT MOST PEOPLE MISS

Financial commentators assume that buyers in the TBA market are being scammed by the cheapest-to-deliver mechanic, receiving fundamentally inferior assets. They miss the calculated paradox of adverse selection: buyers actively accept the lowest-quality pools precisely because the extreme liquidity of the TBA contract overcompensates for the fundamental asset weakness.

Sophisticated originators actively weaponize this system. They use algorithmic models to sift through thousands of mortgages, pulling out the highly valuable loans—such as those with low prepayment risk—and selling them separately in the customized “specified pool” (SP) market for a premium. They then dump the remaining low-value dregs into the TBA market. If algorithms become too efficient at stripping out all the high-quality loans, the baseline quality of the TBA market degrades, threatening the fungibility illusion that keeps the entire global mortgage engine running.

THE TRAJECTORY

Next 12–36 Months: Major electronic trading platforms will implement continuous algorithmic netting, allowing institutional dealers to offset massive TBA positions instantly without requiring the physical delivery of millions of individual mortgage pools.

Next Five Years: Artificial intelligence will completely automate specified pool extraction. Originators will use neural networks to predict borrower prepayment behavior with extreme accuracy, systematically routing every single high-value loan away from the TBA market to capture maximum premium yields.

Next Ten Years: Regulatory bodies will force the transition of TBA settlements onto distributed ledger architectures. Tokenized forward contracts will allow for instantaneous atomic settlement, eliminating the legacy forty-eight-hour announcement window and drastically reducing counterparty credit risk across the financial system.

What Could Go Wrong: A sudden breakdown in the mathematical fungibility of the Uniform Mortgage-Backed Security (UMBS) platform. If investors determine that Fannie Mae pools consistently prepay faster than Freddie Mac pools, they will refuse to treat them interchangeably, immediately fracturing the TBA market’s liquidity and causing a violent spike in consumer mortgage rates.

Most Likely Outcome: The TBA market will remain the undisputed mechanism for global mortgage liquidity. However, it will increasingly function as a purely synthetic hedging and rate-locking tool, with actual physical delivery of premium mortgage assets moving permanently to the specified pool market.

KEY TERMS

- To-Be-Announced (TBA) Trade: A forward-settling financial transaction where the buyer and seller agree on the broad terms of a mortgage-backed security without specifying the exact asset until right before delivery.

- Cheapest-to-Deliver: A pricing dynamic where the seller intentionally delivers the lowest-value asset that legally satisfies the broad parameters of a standardized forward contract.

- Fungibility: The fundamental economic assumption that individual financial assets, such as distinct mortgage pools, are perfectly interchangeable for trading purposes.

- Specified Pool (SP): A distinct, explicitly identified mortgage-backed security traded outside the TBA market because its superior prepayment characteristics command a higher price.

- Uniform Mortgage-Backed Security (UMBS): A consolidated financial instrument designed to make Fannie Mae and Freddie Mac mortgage pools perfectly interchangeable within the TBA trading ecosystem.

SOURCES

- Securities Industry and Financial Markets Association (SIFMA) — Uniform Practices Manual for the Clearance and Settlement of Mortgage-Backed Securities

- Federal Reserve Board — Cheapest-to-Deliver Pricing, Optimal MBS Securitization, and Market Quality

- Federal Reserve Bank of New York — TBA Trading and Liquidity in the Agency MBS Market

- Ginnie Mae — The Past, Present and Future of Agency MBS Liquidity