Advertisement

)

AT A GLANCE

- Concept: Real-Time Settlement: Trillions of euros move instantly across European borders through decentralized central bank ledgers.

- Concept: Interbank Failure: When private banks stop lending to each other, central banks absorb the cross-border transaction risks.

- Concept: Accounting Fiction: National central bank imbalances operate as perpetual, interest-bearing claims without a maturity date.

- Concept: Capital Flight: TARGET2 claims highlight exactly how much private wealth has structurally migrated out of peripheral European economies.

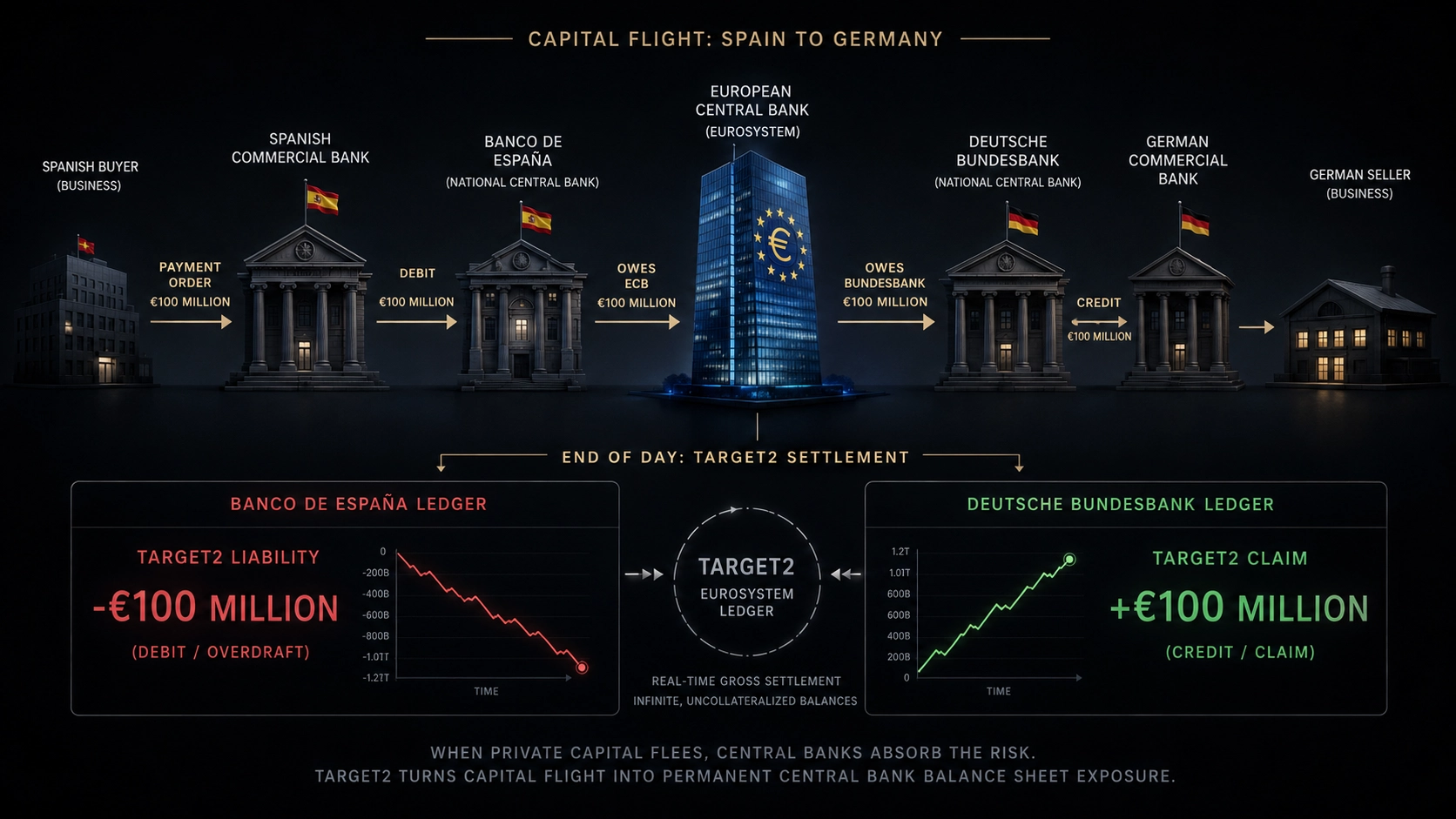

HOW IT WORKS

When a Spanish business buys machinery from a German manufacturer, euros must physically shift jurisdictions. The Spanish buyer tells their local commercial bank to transfer funds to the German seller’s bank. In a healthy economy, these cross-border private bank flows naturally offset each other through commercial interbank lending.

When private trust evaporates, this decentralized offsetting completely breaks down. The European Central Bank solves this through the Trans-European Automated Real-time Gross settlement Express Transfer (TARGET2, recently modernized to T2) system. Instead of the Spanish commercial bank paying the German commercial bank directly, the settlement routes through their respective National Central Banks.

The Banco de España debits the Spanish buyer’s bank account and mathematically owes the money to the European Central Bank. The European Central Bank simultaneously owes the money to the Deutsche Bundesbank. Finally, the Bundesbank credits the German seller’s local commercial bank with newly created central bank reserves.

At the end of the business day, the European Central Bank nets out all these bilateral transactions. If more money flowed into Germany than flowed out, the Bundesbank registers a positive TARGET2 claim on the Eurosystem. Conversely, the Banco de España registers a negative TARGET2 liability, creating a massive, indefinite central bank overdraft that legally balances the Eurozone’s books.

WHY IT MATTERS NOW

Mainstream economists frequently dismiss TARGET2 imbalances as a harmless accounting identity. This ignores the stark geopolitical reality of Eurozone wealth distribution. These balances represent a massive, silent bailout mechanism operating entirely outside the democratic legislative process.

During periods of sovereign debt stress or regional banking panic, depositors pull their euros out of Italian or Greek banks and wire them to perceived safe havens in Frankfurt or Luxembourg. To fund this massive capital flight, peripheral banks must borrow heavily from their local central banks using low-quality collateral.

The TARGET2 system forces the core nations to accept this flight capital without friction. When a core central bank like the Bundesbank creates reserves to finalize these incoming transfers, it effectively extends a direct, uncollateralized loan to the rest of the Eurosystem. The core country exports physical goods and stability, and in return, it receives a digital ledger entry at the European Central Bank.

For the German Bundesbank, this dynamic creates an astronomical financial exposure. Germany’s TARGET2 claims routinely exceed one trillion euros, representing over a quarter of the country’s entire net international investment position. If a peripheral nation defaults or exits the Eurozone, these unbacked TARGET2 liabilities could instantly evaporate, leaving the Bundesbank with a catastrophic, trillion-euro hole in its balance sheet.

This asymmetrical liquidity trap fundamentally alters European monetary policy. The European Central Bank cannot easily raise interest rates or aggressively shrink its balance sheet without triggering a peripheral banking collapse. The sheer size of TARGET2 liabilities forces the Eurosystem to continually accommodate weaker southern economies to prevent the entire currency union from structurally tearing itself apart.

WHAT MOST PEOPLE MISS

Financial media assumes that euros held in an Italian bank are identical to euros held in a German bank. They miss the reality that TARGET2 imbalances mathematically prove a creeping fragmentation of the single currency. When capital flees, the peripheral central bank is essentially printing local euros to replace the ones that left, replacing private commercial money with central bank credit.

This dynamic operates as a massive, stealth debt-restructuring program. Southern European nations are effectively financing their structural current account deficits by running up infinite, non-repayable overdrafts on the Eurosystem ledger. They purchase foreign goods and assets not by exporting their own competitive products, but by expanding their central bank liabilities.

The core nations are forced to continuously extend this credit indefinitely. If a creditor like Germany demanded actual repayment, it would immediately trigger the sovereign defaults and currency collapse it spent decades trying to prevent. The supposed strength of the Eurozone actually relies entirely on the universal agreement to never settle the bill.

THE TRAJECTORY

Next 12–36 Months: The European Central Bank will implement stricter collateral haircuts for peripheral banks accessing the central liquidity management framework. This will attempt to cap the growth of target liabilities by physically restricting how much fresh liquidity struggling national banks can draw to fund outward capital flight.

Next Five Years: The complete modernization of the T2 platform will integrate automated, real-time analytics to flag unnatural sovereign capital migrations. European regulators will utilize this granular telemetry to preemptively identify localized bank runs before they register as macroscopic, trillion-euro central bank imbalances.

Next Ten Years: The introduction of a retail Digital Euro will bypass the commercial banking settlement layer entirely. Direct citizen-to-central-bank wallets will force the Eurosystem to fundamentally redesign cross-border ledger clearing, potentially eliminating the national central bank intermediary model that generates localized TARGET2 claims.

What Could Go Wrong: If a major peripheral economy elects a populist government that threatens to unilaterally exit the Eurozone, capital flight will accelerate exponentially. The resulting hyper-expansion of TARGET2 liabilities would mathematically force the Eurosystem to freeze cross-border electronic payments, instantly destroying the single currency’s fungibility.

Most Likely Outcome: TARGET2 imbalances will become a permanent, ever-expanding fixture of the Eurozone architecture. The political impossibility of settling these trillion-euro ledgers ensures they will function indefinitely as the silent structural glue holding the fractured European banking system together.

KEY TERMS

- TARGET2 (T2): The European Central Bank’s centralized real-time gross settlement network used to process large-value cross-border euro transactions.

- Capital Flight: The rapid, large-scale movement of private financial assets out of a structurally weak national economy into a perceived safe-haven jurisdiction.

- Real-Time Gross Settlement (RTGS): A payment architecture where interbank transactions are cleared and settled individually and instantly, rather than being netted at the end of the day.

- Central Liquidity Management (CLM): The core Eurosystem module where national central banks settle monetary policy operations and manage minimum reserve requirements.

- Net International Investment Position (NIIP): The overall mathematical difference between a nation’s total external financial assets and its total external liabilities.

SOURCES

- European Central Bank (ECB) — TARGET Balances and Central Liquidity Management Architecture

- Deutsche Bundesbank — The Dynamics of TARGET2 Claims and Cross-Border Asset Risks

- Banque de France — The Accounting and Economic Implications of Eurosystem Liquidity Circulation

- Ifo Institute for Economic Research — The Economics of TARGET Balances and Sovereign Debt Restructuring