Advertisement

)

AT A GLANCE

- Concept: Central Novation: The clearinghouse legally inserts itself between buyers and sellers to guarantee trade settlement.

- Concept: Multilateral Netting: Algorithms mathematically cancel offsetting bond purchases and sales to minimize capital transfer requirements.

- Concept: Margin Haircuts: The system calculates strict cash deposit requirements based on the un-netted directional risk.

- Concept: Liquidity Throttling: Algorithm-driven margin adjustments can instantly freeze or expand institutional funding capacity globally.

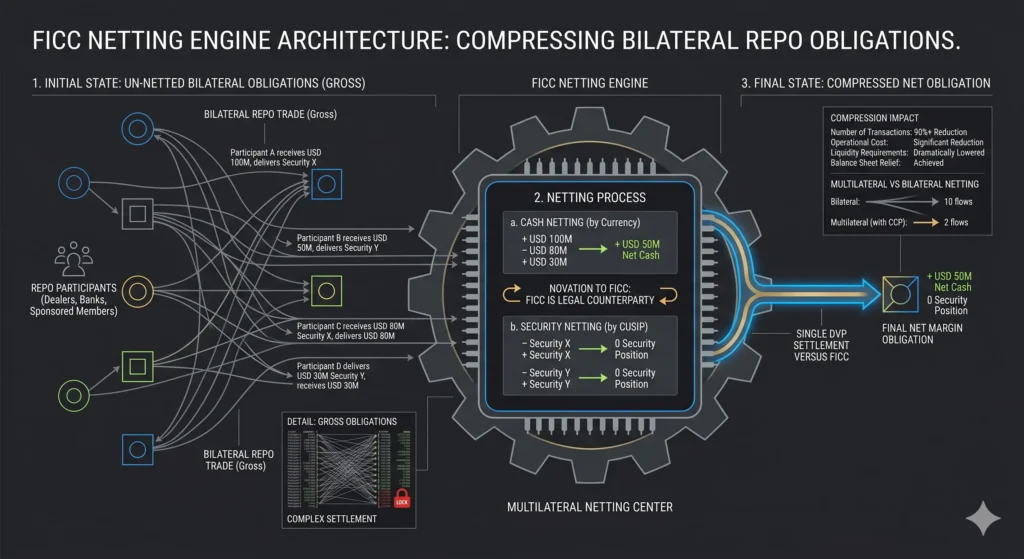

HOW IT WORKS

The global financial system requires constant access to short-term cash to function. Institutional investors obtain this cash through repurchase agreements, selling United States Treasury bonds to a counterparty with a strict legal promise to buy them back the next day.

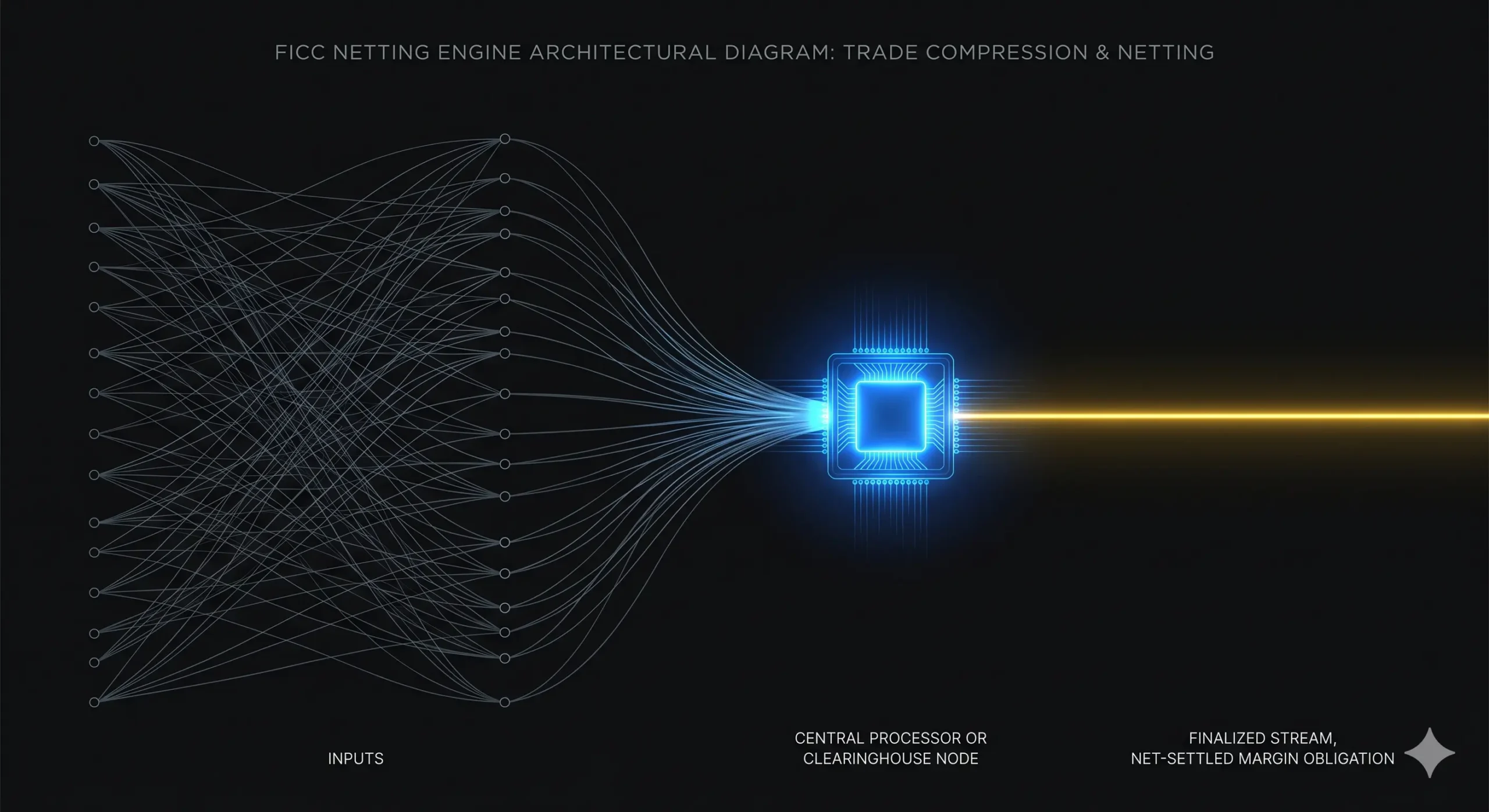

Managing millions of these bilateral agreements manually would exhaust the balance sheet capacity of every major bank. The Fixed Income Clearing Corporation (FICC) operates an automated engine to solve this exact mathematical bottleneck. As trades occur, the FICC executes a legal novation, becoming the buyer to every seller and the seller to every buyer.

Once novated, the engine runs a continuous multilateral netting algorithm. If a broker-dealer buys ten billion dollars of a specific Treasury bond and sells nine billion dollars of that identical security across dozens of different clients, the engine cancels the overlapping volume. The dealer only settles a one-billion-dollar net obligation.

To protect the market from a sudden banking default, the engine demands a daily clearing fund deposit. The system calculates this margin using a historical Value at Risk (VaR) model:

$$VaR = Z \times \sigma \times \sqrt{t} \times V$$

Where Z represents the required statistical confidence level, σ (sigma) is the historical price volatility of the bond, t is the settlement time horizon, and V is the net exposure value. This mathematical formula dictates exactly how much cash a bank must surrender to the clearinghouse to participate in the overnight funding market.

WHY IT MATTERS NOW

The United States government funds its structural deficits by issuing unprecedented volumes of sovereign debt. Primary dealers must absorb this issuance, heavily relying on the repo market to finance their mandatory Treasury purchases.

The Securities and Exchange Commission recently mandated that a significantly larger portion of all Treasury cash and repo trades must clear centrally through the FICC. This regulatory shift forces previously exempt hedge funds, proprietary trading firms, and foreign central banks into the automated netting engine.

When extreme macroeconomic shocks hit the bond market, the VaR formula detects the rising volatility and automatically increases the margin requirement. In March 2020, as pandemic fears triggered a massive global dash for cash, the FICC engine algorithmically spiked clearing fund requirements to protect the central counterparty.

This automated margin call acts as a brutal systemic throttle. If the clearinghouse demands an extra ten billion dollars in margin, dealers must instantly pull that cash out of the broader economy. The mathematical safety mechanism of the netting engine directly dictates the absolute speed limit of global credit creation.

WHAT MOST PEOPLE MISS

Financial media typically reports total Treasury issuance as a simple measure of government borrowing capacity. They completely miss that the FICC netting engine physically controls whether the banking sector can actually afford to hold that debt overnight.

A microscopic change in the FICC margin haircut formula ripples instantly through the shadow banking system. Because dealers use netted Treasury positions to secure cheap funding, an algorithmic decision to increase the haircut by just one percent permanently erases trillions of dollars in systemic institutional purchasing power.

THE TRAJECTORY

Next 12–36 Months: The SEC central clearing mandate will force hundreds of non-bank financial institutions to build direct software API pipelines into the FICC. This integration will trigger a massive surge in daily margin calls for previously un-netted algorithmic trading firms.

Next Five Years: Cross-margining algorithms will merge cash Treasury positions with interest rate futures managed by the Chicago Mercantile Exchange. This mathematical synchronization will drastically lower the total collateral required to hold complex, multi-exchange sovereign debt portfolios.

Next Ten Years: Quantum computing models will replace historical VaR calculations entirely. The clearinghouse will dynamically assess real-time counterparty credit risk and localized market liquidity, adjusting individual margin requirements on a minute-by-minute basis.

What Could Go Wrong: A sudden, unprecedented algorithmic flash crash in the Treasury market could exceed the historical volatility parameters of the VaR model. The resulting margin shortfall would force the FICC to liquidate a defaulting member’s massive bond portfolio into a crashing market, accelerating a systemic collapse.

Most Likely Outcome: The FICC netting engine will consolidate its position as the ultimate central nervous system of United States sovereign debt. Total central clearing will reduce daily settlement failures but permanently increase the baseline cost of capital for all high-frequency bond traders.

KEY TERMS

- Repurchase Agreement (Repo): A short-term financial contract where an institution sells a security and agrees to buy it back at a higher price the following day.

- Novation: The legal mechanism where a central clearinghouse substitutes itself as the buyer to every seller and the seller to every buyer.

- Value at Risk (VaR): A statistical risk management metric that calculates the maximum potential financial loss a specific portfolio could suffer over a given timeframe.

- Multilateral Netting: An automated algorithmic process that aggregates and cancels out overlapping financial transactions among multiple parties to establish a single delivery obligation.

- Haircut: The percentage difference between the current market value of an asset and the value assigned to that asset when used as collateral for a loan.

SOURCES

- Depository Trust & Clearing Corporation (DTCC) — Fixed Income Clearing Corporation Rulebook and Margin Methodology

- Securities and Exchange Commission (SEC) — Standards for Covered Clearing Agencies for U.S. Treasury Securities

- Federal Reserve Bank of New York — The Microstructure of the U.S. Treasury Repurchase Agreement Market

- Bank for International Settlements (BIS) — Central Clearing and Systemic Risk in Sovereign Debt Markets