Advertisement

)

AT A GLANCE

- Concept: Pro-Rata Bidding requires elite financial institutions to legally bid on every sovereign debt auction.

- Concept: The Auction Tail measures the exact yield penalty when dealers must absorb unwanted debt.

- Concept: Repurchase Agreements allow primary dealers to fund mandatory debt purchases using overnight cash loans.

- Concept: The Standing Repo Facility provides emergency central bank liquidity to prevent systemic dealer insolvency.

HOW IT WORKS

The United States Treasury relies on a highly regulated intermediary network to fund the federal government and refinance maturing obligations. Instead of selling debt directly to individual investors, the Treasury funnels issuance through twenty-four elite global banks and brokerages designated as primary dealers. This concentrated architecture physically controls the distribution of the world’s primary reserve asset.

The Federal Reserve Bank of New York grants this elite status under strict operational and capital constraints. In exchange for exclusive trading access with the central bank, primary dealers accept a brutal underwriting obligation. They must submit reasonably competitive bids for their exact mathematical pro-rata share of every single Treasury auction.

If an auction offers fifty billion dollars in new Treasury notes, each dealer must independently bid for roughly two billion dollars of that issuance. When foreign central banks and domestic mutual funds submit strong bids, the primary dealers buy very little. The auction clears smoothly at a low yield, and the global financial system functions normally.

When end-investor demand collapses, the mathematical obligation forces the primary dealers to catch the falling knife. The dealers must purchase the unwanted bonds to guarantee the auction does not physically fail. This emergency absorption immediately bloats the balance sheets of the primary dealers with billions of dollars in illiquid sovereign debt.

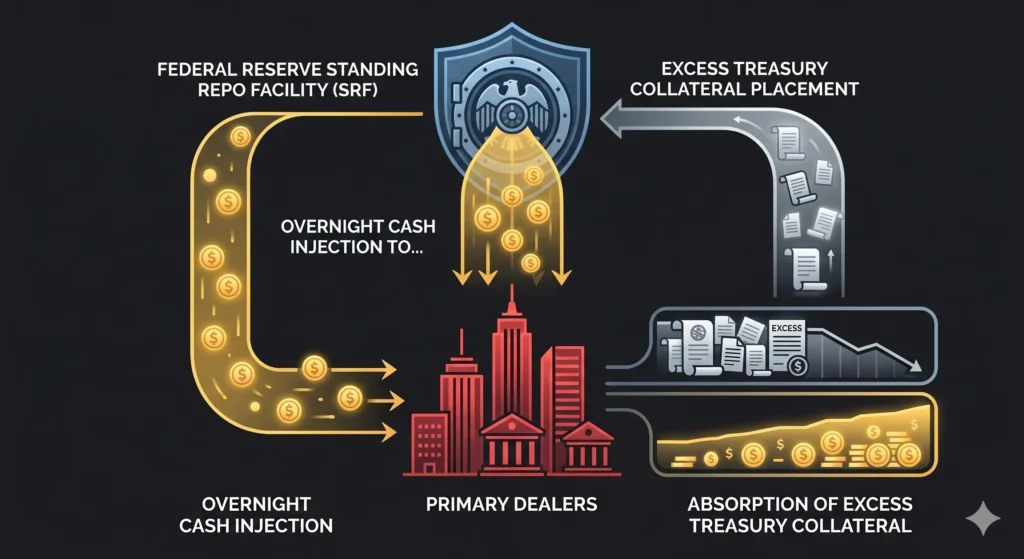

To finance these massive, unexpected bond purchases, primary dealers rely heavily on the overnight repurchase agreement market. They pledge the newly acquired Treasury bonds as collateral to clearing banks and money market funds in exchange for short-term cash. The dealers then use this borrowed cash to finalize settlement with the Treasury, closing the auction loop.

WHY IT MATTERS NOW

The United States government runs unprecedented structural deficits, requiring the Treasury to issue trillions of dollars in new debt annually. This sheer volume places immense strain on the primary dealer network. The aggregate balance sheet capacity of these two dozen institutions dictates the absolute speed limit of federal deficit spending.

During periods of high inflation and rising interest rates, institutional investors frequently boycott long-duration Treasury auctions. This buyers’ strike forces primary dealers to absorb a record share of the debt issuance. When dealers absorb excessive debt, they exhaust their balance sheet capacity to warehouse further risk, threatening the structural stability of the broader financial system.

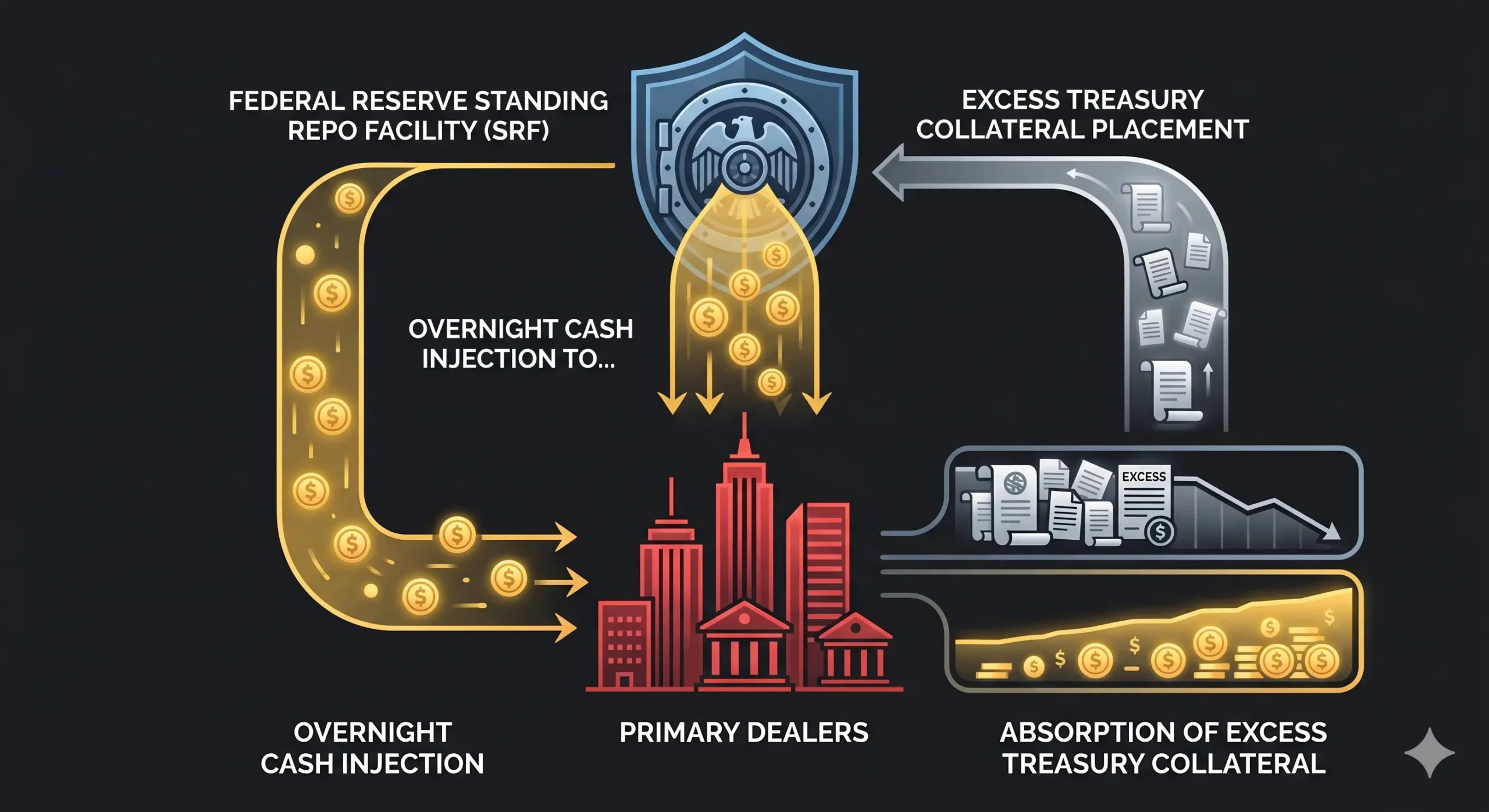

If primary dealers cannot secure overnight cash to fund their mandatory auction purchases, the repo market instantly freezes. This scenario occurred catastrophically in early 2020 when pandemic panic caused extreme institutional liquidity hoarding. Primary dealers held billions in pristine Treasury bonds but faced imminent bankruptcy because private entities simply refused to lend them cash.

To prevent a sovereign debt crisis, the Federal Reserve institutionalized the Standing Repo Facility to backstop the primary dealer network permanently. This mechanism acts as the ultimate systemic safety valve. When private lending disappears, the central bank steps in directly to lend infinite cash against Treasury collateral.

This central bank backstop effectively subsidizes the federal deficit. By guaranteeing that primary dealers never run out of cash to buy new bonds, the Federal Reserve implicitly underwrites the Treasury auction mechanism. This automated architecture removes true market discipline, allowing the government to issue debt far beyond what organic private demand naturally supports.

WHAT MOST PEOPLE MISS

Standard macroeconomic reports focus entirely on the final yield of a Treasury auction. They treat a rising yield as a simple reflection of future inflation expectations or domestic economic growth. These observations completely miss the underlying mechanical stress hidden within the auction data.

These reports ignore the structural mechanics of the auction tail. The tail measures the exact spread between the expected yield before the auction and the highest yield the Treasury must accept to sell the final bond. A widening tail indicates that organic demand has evaporated and the Treasury is forcing the primary dealers to absorb the excess issuance at a severe penalty rate.

Analysts assume primary dealers operate as omnipotent market makers capturing risk-free arbitrage. In reality, strict post-crisis banking regulations penalize these institutions for holding too many safe Treasury bonds on their balance sheets. The government forces dealers to buy the debt during weak auctions, then legally penalizes the banks for hoarding the assets, creating a severe structural paradox at the core of global capital markets.

THE TRAJECTORY

Next 12–36 Months: The Securities and Exchange Commission will mandate central clearing for all Treasury market transactions. This operational shift will compress the margin requirements for primary dealers and force non-dealer trading firms to absorb more settlement risk.

Next Five Years: The Treasury Department will increasingly rely on short-term Treasury bills rather than long-term bonds to fund deficits. This duration shift will heavily saturate money market funds and require continuous daily refinancing operations across the dealer network.

Next Ten Years: The Federal Reserve will expand emergency repo facilities to include a wider range of non-bank financial institutions. This structural expansion will socialize the liquidity backstop, reducing the Treasury’s absolute dependence on the balance sheets of the traditional banking oligopoly.

What Could Go Wrong: A sudden downgrade in sovereign credit quality could trigger an algorithmic selloff across global bond markets. A coordinated dealer strike during a major auction would cause the first outright failure of a United States Treasury debt issuance.

Most Likely Outcome: The primary dealer network will remain the indispensable shock absorber of sovereign finance. The Federal Reserve will continually expand its emergency repo facilities to ensure these institutions possess infinite liquidity, effectively merging monetary policy and debt distribution.

KEY TERMS

- Primary Dealer: A pre-approved financial institution holding a legal obligation to underwrite sovereign debt auctions directly with a central bank.

- Pro-Rata Share: The exact mathematical percentage of a Treasury auction that an individual dealer must bid for to fulfill its legal obligations.

- Auction Tail: The basis point difference between the expected market yield of a bond immediately prior to an auction and the actual highest yield accepted.

- Standing Repo Facility: A permanent central bank mechanism that lends overnight cash against high-quality collateral to prevent liquidity shortages in the financial system.

- Basel III Constraint: A post-crisis banking regulation requiring financial institutions to hold unweighted capital against all assets, penalizing large inventories of low-yielding sovereign debt.

SOURCES

- Federal Reserve Bank of New York — Administration of Relationships with Primary Dealers

- United States Department of the Treasury — Treasury Auction Mechanics and Bidding Rules

- Bank for International Settlements — Dealer Constraints and the Microstructure of Sovereign Debt Markets

- Congressional Budget Office — The Economic Impact of Structural Deficits on Treasury Auction Volatility