Advertisement

)

AT A GLANCE

- Concept: Electronic Matching: Algorithms continuously pair cross-border transaction instructions using automated communications protocols.

- Concept: Settlement Windows: Dedicated daytime and overnight processing cycles dictate when assets officially change ownership.

- Concept: Delivery Versus Payment: The pipeline synchronizes the exact moment a security transfers against cash.

- Concept: Collateral Gridlock: Timing asymmetries between the two depositories trap high-quality liquid assets mid-transfer.

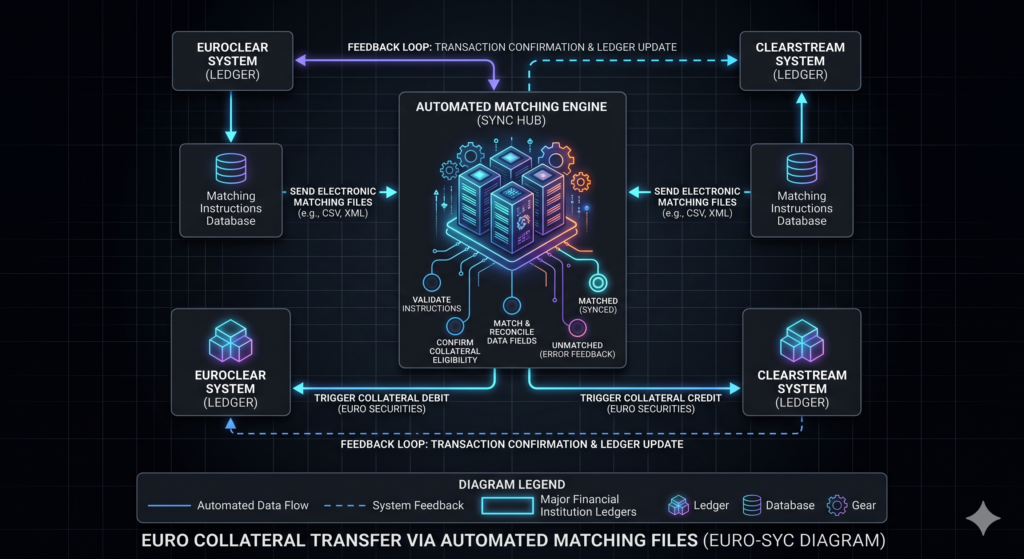

HOW IT WORKS

European capital markets rely on two massive offshore vaults to hold trillions in sovereign debt and equities: Euroclear Bank in Belgium and Clearstream Banking in Luxembourg. These International Central Securities Depositories (ICSDs) operate entirely separate digital ledgers. When a client at Euroclear trades with a client at Clearstream, the assets cannot simply change accounts internally.

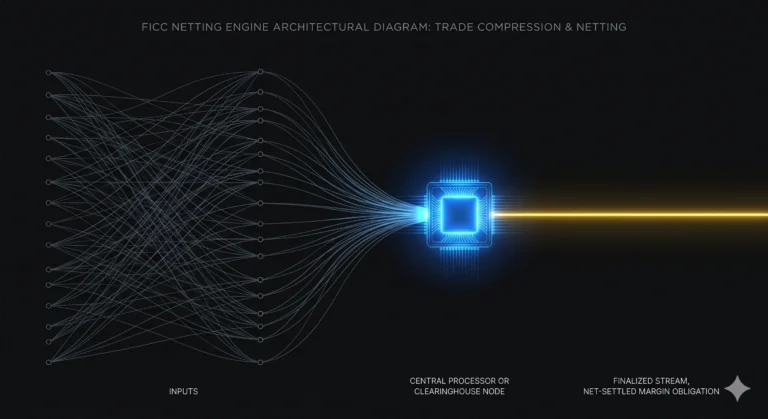

The financial system bridges this gap using a highly specialized electronic pipeline known simply as the Bridge. This digital infrastructure facilitates the exchange of delivery and feedback files across secure networks. Transactions execute strictly under the Delivery-Versus-Payment model to eliminate principal risk.

The process begins with the exchange of inter-ICSD matching transmissions. These rolling communications run constantly from early morning until late evening. The software algorithms require both the buyer and the seller to submit identical trade details to initiate a settlement cycle.

Once the system matches the instructions, the delivering depository verifies that the client holds the required securities. The receiving depository simultaneously verifies the buyer holds the requisite commercial bank money.

The Bridge then executes the transfer in synchronized batches. It adjusts internal credit lines and debits accounts simultaneously across international borders. The receiving entity gets absolute confirmation through specific feedback messages, permanently closing the settlement loop.

WHY IT MATTERS NOW

Global finance operates on the continuous mobilization of collateral. Hedge funds, pension managers, and commercial banks use high-quality sovereign debt to secure overnight cash in the repurchase agreement (repo) market. This market requires assets to move flawlessly between counterparty accounts within hours.

The transition to a T+1 settlement cycle severely compresses the operational window for this global collateral mobilization. Market participants now possess a fraction of the historical timeframe to locate, match, and transfer securities.

If a European repo trade involves parties split across Euroclear and Clearstream, the Bridge becomes the absolute physical bottleneck for the transaction. Software must reconcile the dual ledger entries flawlessly before the daily cut-off times expire.

When European regulators enforced the Central Securities Depositories Regulation (CSDR), they introduced strict financial penalties for settlement failures. A delayed transfer across the Bridge now results in immediate, compounding cash fines for the failing institution.

This mechanical reality concentrates systemic risk within the inter-depositary communication files. If a single large sovereign bond transfer stalls in the Bridge, the receiving bank cannot use that asset to fund its own downstream obligations. A local technical delay instantly metastasizes into a multi-billion-euro liquidity shortfall across the broader European banking network.

WHAT MOST PEOPLE MISS

Standard financial overviews treat Euroclear and Clearstream as a unified, frictionless European back office. They assume a matched trade guarantees an instantaneous electronic handover. They ignore the precarious timing asymmetries embedded in the separate operating schedules of the two depositories.

Each depository executes its own partial settlement runs, overnight processing windows, and final intraday cut-offs at slightly different times. These disjointed schedules create isolated dead zones in the daily processing cycle. An instruction sent during a processing pause simply queues in the server, generating no immediate action.

If a seller in Clearstream misses the specific cross-border gating event by five minutes, the asset misses the batch transfer file. The security remains locked in transit logic until the next processing window opens.

During extreme market stress, this simple scheduling asymmetry traps billions of euros in collateral mid-flight. The delay forces desperate banks to borrow emergency cash at punitive interest rates while they wait for the software ledgers to synchronize.

THE TRAJECTORY

Next 12–36 Months: Operators will compress the rolling file exchange frequencies to near real-time intervals. This update will align the Bridge with stringent T+1 settlement requirements, minimizing the duration assets spend locked in cross-border transit status.

Next Five Years: Regulatory bodies will force the ICSDs to standardize their internal partial settlement windows. Exact synchronization of these processing cycles will drastically reduce the margin of error for automated trading firms managing high-velocity repo collateral.

Next Ten Years: The legacy file-batching architecture will transition to a distributed ledger or unified atomic settlement network. This structural shift will merge the two distinct ledgers mathematically, effectively dissolving the need for a discrete communication bridge.

What Could Go Wrong: A severe cyberattack targeting the inter-ICSD matching transmissions would sever the primary artery of European finance. Without the Bridge confirming transfers, the entire cross-border repo market would instantly freeze, causing widespread counterparty defaults within twenty-four hours.

Most Likely Outcome: The Bridge will remain the central nervous system of European cross-border settlement. The ICSDs will incrementally optimize the pipeline’s speed, but fundamental data silos will persist until central banks mandate a unified digital currency settlement rail.

KEY TERMS

- International Central Securities Depository (ICSD): A financial institution that holds securities globally and facilitates the clearing and settlement of international trades.

- Delivery-Versus-Payment: A settlement mechanism that ensures the transfer of securities only occurs if the corresponding payment occurs simultaneously.

- Repurchase Agreement (Repo): A short-term borrowing contract where a party sells securities and agrees to buy them back later at a slightly higher price.

- Central Securities Depositories Regulation (CSDR): A European Union directive designed to increase the safety and efficiency of securities settlement and penalize trade failures.

- Settlement Gating Event: A strict chronological deadline within a clearing system that determines if a transaction enters the current processing batch or delays to the next.

SOURCES

- Clearstream Banking Luxembourg — Client Operational Handbook and Bridge Timings Matrix

- Euroclear Bank SA/NV — Settlement Services and Cross-Border Interoperability Guidelines

- European Securities and Markets Authority (ESMA) — CSDR Settlement Discipline Regime Reports

- Bank for International Settlements (BIS) — The Microstructure of Cross-Border Securities Settlement