Advertisement

)

AT A GLANCE

- Concept: Electronic Warranting: A secure digital ledger tracks absolute title ownership of standardized 25-tonne physical copper lots.

- Concept: Visible Inventory: Published daily stock levels establish a psychological baseline for global industrial manufacturing supply availability.

- Concept: Warrant Cancellation: Traders electronically earmark specific metal for withdrawal, instantly shrinking the tradable global exchange supply.

- Concept: Arbitrage Squeeze: Commodity houses weaponize localized warehouse rules to orchestrate massive withdrawals and artificially inflate spot premiums.

HOW IT WORKS

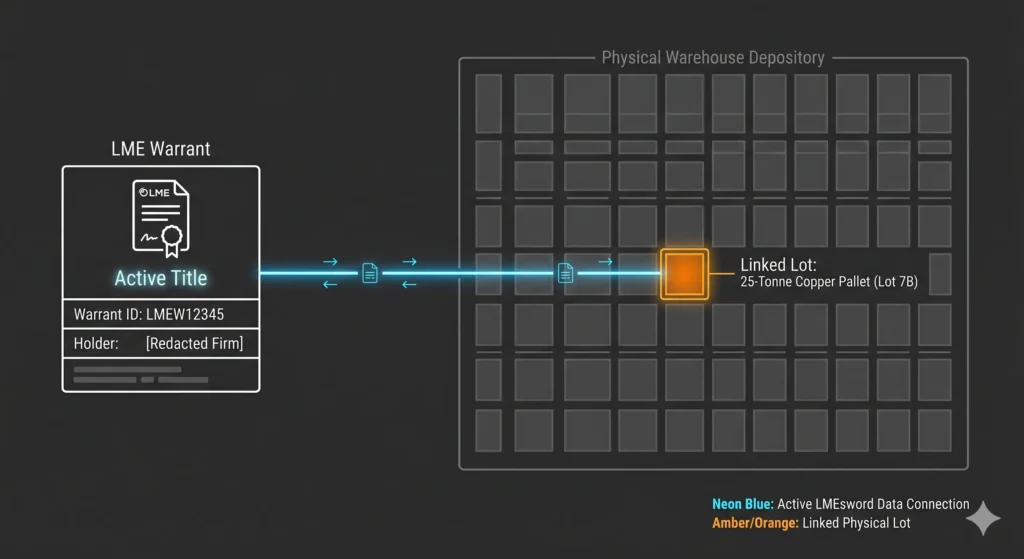

The global copper market does not trade amorphous financial concepts; it trades physically standardized cathodes. For an institution to settle a contract on the London Metal Exchange (LME), they must deliver an LME Warrant. This warrant is a highly secure legal document representing absolute title ownership over a specific 25-tonne lot of 99.99 percent pure copper securely sitting inside one of over six hundred exchange-approved global warehouses.

Through a centralized electronic depository system known as LMEsword, traders instantly transfer possession of these massive metal stockpiles around the world without ever physically moving the underlying cargo. The digital ledger accounts for every tonne of metal registered on the exchange, making it immediately available to back the millions of futures contracts traded daily.

The strict standardization of these warrants guarantees absolute fungibility. A trader buying copper in London knows precisely that the metal sitting in an approved warehouse in Rotterdam meets the exact chemical purity requirements dictated by the exchange. This physical assurance allows global financial institutions to use warehouse warrants as pristine collateral for multi-billion-dollar overnight lending agreements.

When an industrial consumer or an arbitrage trader actually needs the physical metal, they execute a warrant cancellation. This digital command permanently extinguishes the LME title and earmarks the specific 25-tonne lot for physical load-out onto a shipping vessel. The metal does not instantly vanish from the warehouse, but it officially exits the exchange’s visible, tradable inventory.

This cancellation mechanism triggers the fundamental economics of base metal price discovery. The LME publishes the exact volume of cancelled warrants daily, telegraphing real-time physical demand to the entire financial system. Algorithmic trading models scan these daily cancellation reports, dynamically adjusting global spot prices based on the dwindling availability of unallocated metal remaining inside the approved storage network.

WHY IT MATTERS NOW

The energy transition requires an unprecedented volume of physical copper to manufacture electric vehicle motors, wind turbines, and hyperscale data center transformers. As structural deficits loom, the LME warehouse network serves as the ultimate barometer of global industrial starvation. If visible exchange inventories fall below extreme thresholds, it proves the mining sector can no longer satiate global manufacturing demand.

Commodity trading behemoths like Trafigura weaponize this exact ledger transparency to orchestrate massive cross-exchange arbitrage opportunities. If prices in a competing market—such as the COMEX in New York or the Shanghai Futures Exchange—spike higher than London, traders systematically cancel massive tranches of LME warrants. They physically load the copper onto ships and redirect it to the more lucrative geographic zone to capture the massive spread.

This withdrawal mechanic actively drains the LME of its structural liquidity buffer. During a recent structural dislocation, major commodity houses cancelled over 50,000 tonnes of copper warrants in a single trading session, dragging LME visible stocks to their lowest levels since 1974. When this massive withdrawal printed on the daily exchange report, it immediately triggered a violent short squeeze, driving the spot price up by thirteen percent.

The sudden disappearance of visible metal traps financial speculators holding short positions. Because LME contracts mandate physical delivery, a trader caught without metal during a severe stock drawdown must scramble to buy available supply at any price to fulfill their legal obligations. This panic buying creates a positive feedback loop, accelerating the price spike and forcing even more catastrophic liquidations across the trading floor.

The geopolitical consequences extend entirely to the industrial base. Manufacturers relying on just-in-time supply chains face catastrophic spot premiums when the LME visible inventory collapses. The sheer threat of further warrant cancellations forces industrial buyers into panic hoarding, perpetually elevating the baseline cost of raw materials required to execute national electrification mandates.

WHAT MOST PEOPLE MISS

Macroeconomic forecasters plot global copper supply against projected demand, assuming the metal flows unobstructed to wherever the price is highest. They completely miss the brutal logistical choke points artificially created by LME load-out rules. Warehouses legally must load out a strictly capped tonnage of metal per day, meaning a trader who cancels 100,000 tonnes might wait months for the physical cargo to actually leave the port.

This physical load-out queue operates as a hidden financial weapon. By cancelling massive volumes of warrants simultaneously, a dominant trading house intentionally clogs the exit doors of a strategic warehouse. This artificial bottleneck permanently locks up regional metal supply, allowing the trader to temporarily corner the spot market and squeeze desperate counterparties who legally must source immediate physical copper.

Warehouse operators actively incentivize this behavior by offering traders a cut of the storage rent. Because the metal remains physically trapped in the queue, the warehouse continues to charge daily storage fees, sharing the profits with the very trading firm that initiated the massive cancellation. This structural paradox turns the supposedly neutral physical depository into an active, highly lucrative component of the commodity trading strategy.

THE TRAJECTORY

Next 12–36 Months: Industrial hedgers will demand the LME implement stricter daily minimum load-out quotas across all approved warehouse operators. The exchange will aggressively penalize storage facilities that intentionally bottleneck the physical removal of cancelled warrants to collect extended rental fees.

Next Five Years: Global commodity traders will shift away from legacy European storage hubs to newly approved LME delivery points across Asia and the Middle East. This geographical pivot will perfectly align physical warrant liquidity with the massive battery manufacturing complexes dominating the Eastern hemisphere.

Next Ten Years: Distributed ledger technology will replace the centralized LMEsword depository completely. Instantaneous, blockchain-verified warrant transfers will allow automotive manufacturers and power utilities to execute peer-to-peer physical copper settlements, entirely bypassing the intermediary fees of global commodity brokers.

What Could Go Wrong: A coordinated hacking attack against the LMEsword digital ledger could temporarily erase the ownership records of trillions of dollars in physical metal. If traders cannot mathematically prove their title to the underlying copper, global banks will instantly freeze all base metal credit lines, completely paralyzing the industrial supply chain.

Most Likely Outcome: The LME warrant system will maintain its absolute monopoly over international base metal price discovery. Despite the rise of competing regional exchanges, the unmatched legal security of the London physical delivery mechanism will guarantee its status as the default collateral ledger for the renewable energy transition.

KEY TERMS

- Warrant: A secure, digital document of title representing absolute legal ownership of a specific, standardized lot of physical metal stored in an exchange-approved warehouse.

- Cancellation: The formal electronic process of earmarking a specific warrant for physical withdrawal, instantly removing that metal from the tradable exchange inventory.

- LMEsword: The centralized electronic depository system operated by the London Metal Exchange to securely track, transfer, and cancel digital metal warrants globally.

- Short Squeeze: A rapid price surge triggered when market participants who bet against an asset must desperately buy it back to cover their failing positions.

- Spot Premium: The additional financial charge a buyer must pay above the standard futures price to secure the immediate physical delivery of a commodity.

SOURCES

- London Metal Exchange (LME) — Policy on the Approval and Operation of Warehouses and Delivery Points

- Bank for International Settlements (BIS) — Central Clearing and Systemic Risk in Commodity Markets

- MDPI Journal of Risk and Financial Management — The Role of Canceled Warrants in the LME Market

- Financial Law Panel — The London Metal Exchange and Documents of Title