Advertisement

)

AT A GLANCE

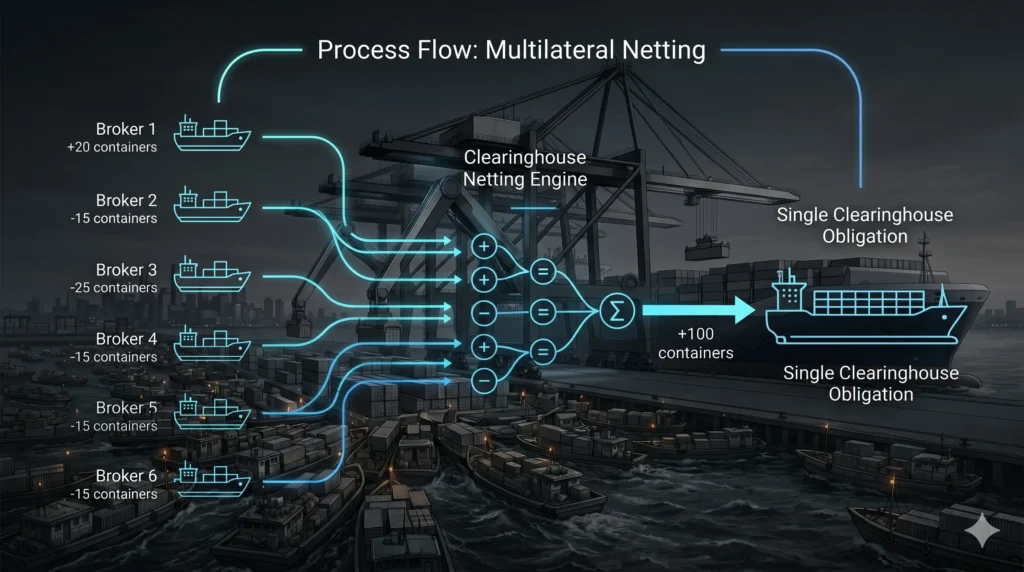

- Concept: Multilateral Netting: The algorithm offsets all daily purchases against all sales for a specific security.

- Concept: Central Counterparty: The clearinghouse steps between buyers and sellers, legally guaranteeing every matched trade.

- Concept: Margin Obligations: Brokers must deposit cash daily based on mathematical models of their un-netted risk.

- Concept: Settlement Compression: Netting eliminates up to 98 percent of the physical capital transfers required daily.

HOW IT WORKS

Retail investors press a button on a brokerage application and assume the stock transfers instantly. In reality, the digital interface simply records a promise. The actual transfer of capital and asset ownership occurs up to 24 hours later through a centralized financial utility.

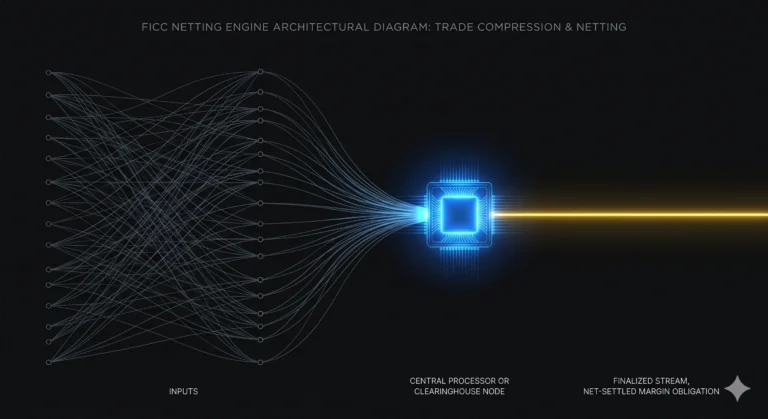

The National Securities Clearing Corporation operates the Continuous Net Settlement engine to process these market promises. Instead of moving cash and shares for every individual trade, the engine waits until the end of the trading session. It aggregates every transaction executed by every participating broker-dealer across the entire market.

The system executes a process called multilateral netting. If a broker buys one million shares of a specific company for various clients and sells nine hundred thousand shares of that same company, the engine mathematically cancels the overlapping volume. The broker only owes a single net settlement of one hundred thousand shares.

To protect the market during the window between trade execution and final settlement, the clearinghouse acts as a central counterparty. It legally becomes the buyer to every seller and the seller to every buyer. This structural insertion isolates the wider financial system from a single broker’s sudden bankruptcy.

Assuming this massive systemic risk requires aggressive capital defense. The engine calculates a daily clearing fund requirement for each broker using sophisticated Value at Risk models. If a broker carries a large, volatile net position overnight, the engine automatically extracts a higher cash margin deposit to guarantee market stability.

WHY IT MATTERS NOW

The transition to a T+1 settlement cycle in North American markets drastically compressed the operational window for global finance. Brokers now have exactly one business day to calculate, locate, and deliver the required capital and securities. This speed forces financial institutions to maintain larger, highly liquid cash buffers at all times.

When extreme market volatility strikes, the margin engine acts as a brutal structural throttle. During retail trading frenzies, brokers routinely face sudden, multi-billion-dollar margin calls from the clearinghouse. The algorithm detects unprecedented directional risk and demands immediate cash to cover potential settlement failures.

Because brokers often lack the unencumbered cash to satisfy the engine’s sudden margin requirement, they must restrict retail buying to lower their risk profile. This mechanical reality proves that capital market access is not determined by public demand, but by automated clearinghouse liquidity formulas. The engine mathematically dictates who can trade during a crisis.

Geopolitically, the efficiency of this settlement infrastructure underpins the dominance of American capital markets. By guaranteeing that trades will settle even if a major counterparty defaults, the engine attracts trillions in foreign sovereign wealth. International capital flows into New York precisely because this automated netting eliminates counterparty credit risk.

WHAT MOST PEOPLE MISS

Public financial commentary assumes a failed trade means a buyer lost their money or a seller lost their stock. In the continuous net settlement system, trade failures are a routine, algorithmically managed mathematical reality. When a broker fails to deliver a stock on settlement day, the system simply rolls the obligation into the next day’s net position.

The engine actively borrows shares from the central depository’s massive inventory to cover these shortfalls temporarily. It charges the failing broker a daily financial penalty and credits the receiving broker. This automated bookkeeping prevents a single localized delivery failure from triggering a cascading freeze across the entire equity network.

If the failure persists beyond a strict regulatory timeframe, the engine executes a mandatory buy-in. It automatically purchases the missing shares on the open market and bills the defaulting broker for the entire cost, neutralizing the systemic risk completely without human intervention.

THE TRAJECTORY

Next 12–36 Months: Regulators will implement stricter intraday margin calculations to protect the clearinghouse. The engine will pull liquidity from broker-dealers multiple times per day based on real-time volatility spikes, permanently increasing the cost of capital for high-frequency trading firms.

Next Five Years: Distributed ledger technology will run in parallel with legacy netting engines to test atomic settlement for specific asset classes. This parallel architecture will completely remove overnight credit risk but demand absolute, pre-funded cash balances before any trade execution.

Next Ten Years: Artificial intelligence will dynamically predict trade failure probabilities based on global macroeconomic indicators. The clearinghouse will preemptively adjust margin requirements for individual securities hours before the volatility actually hits the open market.

What Could Go Wrong: A simultaneous default of several tier-one prime brokers during a severe algorithmic flash crash would exhaust the mutualized clearing fund. The clearinghouse would be forced to liquidate massive equity portfolios into a falling market, accelerating the systemic collapse it was designed to prevent.

Most Likely Outcome: The continuous net settlement system will remain the absolute core of global equities. While the settlement window will shrink, the mathematical efficiency of multilateral netting will prevent the total adoption of purely decentralized, un-netted atomic settlement architectures.

KEY TERMS

- Multilateral Netting: The mathematical aggregation of multiple offsetting transactions between various parties into a single net payment or delivery obligation.

- Central Counterparty (CCP): A financial institution that legally inserts itself between trading parties, guaranteeing the terms of a trade even if one party defaults.

- Value at Risk (VaR): A statistical risk management metric that estimates the maximum potential financial loss a portfolio could suffer over a specific timeframe.

- T+1 Settlement: A regulatory standard requiring stock trades to legally transfer ownership and capital one business day after the initial transaction occurs.

- Clearing Fund: A mutualized pool of cash and highly liquid assets deposited by broker-dealers to absorb losses if a major market participant goes bankrupt.

SOURCES

- Depository Trust & Clearing Corporation (DTCC) — Continuous Net Settlement System Operational Architecture

- Securities and Exchange Commission (SEC) — Risk Management Frameworks for Central Counterparties

- Bank for International Settlements (BIS) — The Role of Margin in Central Clearing and Market Dynamics

- Journal of Financial Market Infrastructures — The Microstructure of Equity Settlement and Trade Failures