Advertisement

)

AT A GLANCE

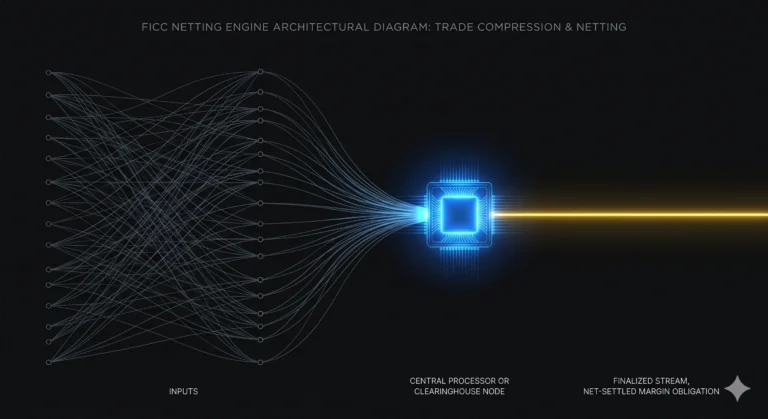

- Concept: Data Aggregation: The engine collects transaction-level clearing data from major overnight repo market platforms.

- Concept: Trimmed Median: Volume-weighted metrics strip away extreme transactional outliers to preserve index calculation stability.

- Concept: Basis Risk: Delays in clearing data transmission cause discrepancies between projected and actual borrowing costs.

- Concept: Settlement Friction: Microsecond mismatches in overnight collateral pricing trigger unexpected institutional liquidity demands.

HOW IT WORKS

The Secured Overnight Financing Rate (SOFR) measures the cost of borrowing cash overnight collateralized by U.S. Treasury securities. The calculation engine processes transaction-level data from three distinct segments of the repurchase agreement market. These segments include the tri-party repo market, the General Collateral Finance market, and the bilateral cleared repo market.

Every business day, the Federal Reserve Bank of New York gathers transaction data directly from clearing banks and fixed-income clearing corporations. The data aggregation pipeline ingests individual trade records containing specific transaction volumes and execution rates. The engine then sorts these transactions from lowest to highest interest rate.

To isolate the benchmark from extreme market anomalies, the engine utilizes a volume-weighted trimmed median calculation. It excludes the lowest 25 percent and the highest 25 percent of dollar-weighted transactions before finalizing the daily rate.

The formula calculates the benchmark based on the surviving middle 50 percent of transactional volume:

Where $R_i$ represents the interest rate of transaction $i$, and $V_i$ represents the matching transaction volume. This math anchors hundreds of trillions of dollars in derivative contracts.

WHY IT MATTERS NOW

The total migration from the London Interbank Offered Rate (LIBOR) to SOFR permanently altered how global capital markets price risk. LIBOR relied on subjective, uncollateralized expert panel estimates from major banks, which invited widespread manipulation. SOFR relies entirely on hard, observable transactions backed by U.S. sovereign debt.

This structural change creates a direct feedback loop between federal monetary policy and private debt markets. When hedge funds execute massive basis trades to arbitrage Treasury futures against cash bonds, they borrow heavily in the overnight repo market. This surging demand for cash instantly drives up the daily SOFR calculation.

During an acute treasury market margin squeeze, such as the liquidity disruptions that locked the market in September 2019, overnight borrowing costs spike unexpectedly. The SOFR engine captures these spikes, causing immediate, automated upward adjustments across corporate loans, credit lines, and consumer mortgages globally.

The speed of modern electronic trading accelerates these adjustments. A sudden liquidity drain in New York instantly changes the cost of capital for corporate borrowers in London or Tokyo, linking global credit availability directly to the daily mechanics of U.S. repo clearinghouses.

WHAT MOST PEOPLE MISS

Academic financial analysis treats SOFR as a flawless, real-time indicator of risk-free capital. This view completely overlooks how the data aggregation pipeline lag introduces basis risk.

The index calculates its rate using transaction data that settled on the previous day, creating a structural settlement lag during rapid market crashes. When clearinghouses experience sudden margin squeezes, operational clearing delays cascade through prime brokerages.

The engine aggregates mismatched data windows, introducing a significant tracking error between the backward-looking index and real-time intraday funding stress.

This basis risk chokes institutional hedging strategies precisely when market volatility peaks, forcing clearing members to clear unexpected settlement gaps using emergency cash pools.

THE TRAJECTORY

Next 12–36 Months: Regulators will press for intraday SOFR updates to mitigate the structural settlement lag. Clearing platforms will deploy real-time telemetry systems to transmit transaction volumes instantly to the Federal Reserve Bank of New York.

Next Five Years: High-frequency trading firms will launch private synthetic indices that predict the daily SOFR print hours in advance. These algorithms will trade on early-session repo platform order books, capturing millions in arbitrage profits before the official benchmark release.

Next Ten Years: The global financial architecture will integrate decentralized ledger systems for instantaneous settlement of sovereign collateral. This will compress the transaction-to-index timeline down to milliseconds, permanently erasing daily basis risk from derivative structures.

What Could Go Wrong: A catastrophic cyberattack or prolonged network outage at a primary clearing node like the Fixed Income Clearing Corporation would halt the data aggregation pipeline entirely. The engine would fail to output the benchmark, freezing automated variable-rate coupon payments globally and triggering mass contractual defaults.

Most Likely Outcome: The backward-looking nature of the index will remain a permanent structural vulnerability. Prime brokerages will build larger cash buffers to absorb the volatile intraday margin calls driven by overnight data aggregation friction.

KEY TERMS

- Secured Overnight Financing Rate (SOFR): A broad measure of the cost of borrowing cash overnight collateralized by U.S. Treasury securities.

- Basis Risk: The financial risk arising from a structural mismatch or pricing discrepancy between two closely related financial instruments or benchmarks.

- Repurchase Agreement (Repo): A short-term contract where one party sells securities to another with an explicit agreement to buy them back at a specified price and date.

- Trimmed Median: A statistical measure of central tendency calculated by removing a predetermined percentage of the lowest and highest values before averaging the remainder.

- Clearinghouse: A centralized financial institution that facilitates the clearing and settlement of transactions, managing counterparty credit risk for participants.

SOURCES

- Federal Reserve Bank of New York — Secured Overnight Financing Rate Data Methodology

- Alternative Reference Rates Committee (ARRC) — Final Report on the Transition from U.S. Dollar LIBOR to SOFR

- Bank for International Settlements (BIS) — The Inherent Vulnerabilities of Overnight Cleared Repo Benchmarks

- Financial Stability Oversight Council (FSOC) — Annual Assessment of Systemic Risk in Short-Term Funding Markets