Advertisement

)

AT A GLANCE

- Concept: Default Sequencing: Losses flow through distinct, predetermined layers of collateral before touching survival capital.

- Concept: Defaulter Resources: The clearinghouse immediately seizes the bankrupt member’s margin and default contributions.

- Concept: Skin in the Game: The exchange sacrifices its own capital tranche before mutualizing losses across competitors.

- Concept: Loss Mutualization: Surviving clearing institutions must deposit emergency cash to absorb remaining systemic losses.

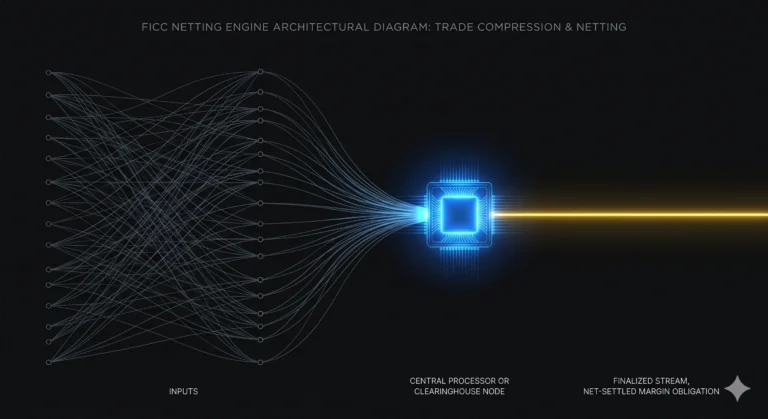

HOW IT WORKS

Central clearinghouses guarantee the structural execution of modern derivatives trading. To eliminate counterparty credit risk, the clearinghouse inserts itself as the buyer to every seller and the seller to every buyer, isolating participants from individual broker bankruptcies.

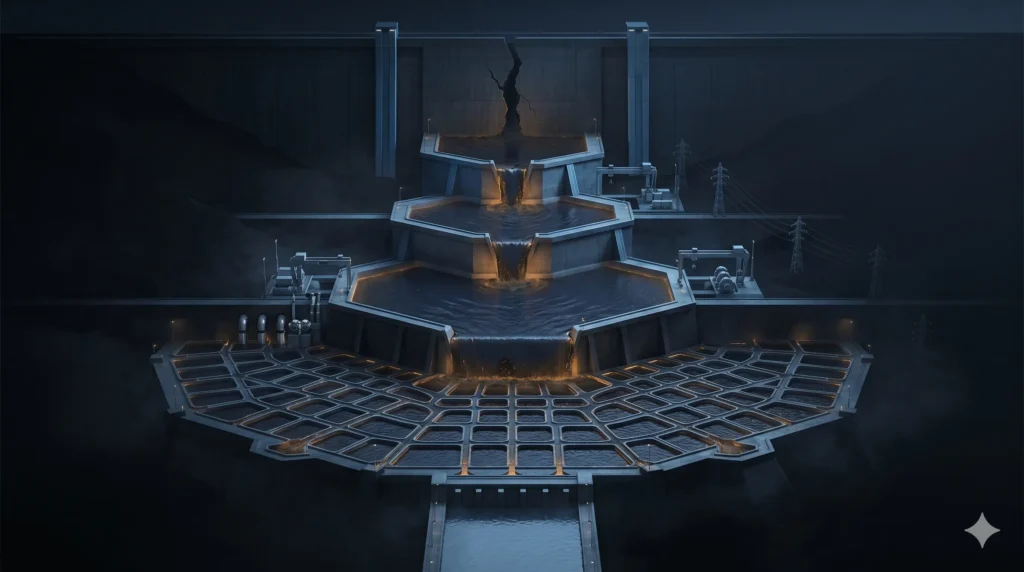

When a massive clearing member defaults due to catastrophic market movements, the clearinghouse must absorb the bankrupt firm’s open, volatile portfolios. It does not absorb these losses on its own balance sheet immediately. Instead, it triggers a mathematical risk-containment process known as the default waterfall.

The default waterfall operates through strict sequential tranches. The clearinghouse first liquidates the defaulting member’s individual proprietary margin and initial margin deposits to cover the immediate deficit. If those assets prove insufficient, the system grabs the defaulting member’s pre-funded contribution to the clearinghouse default fund.

If the losses exceed the defaulter’s total collateral, the clearinghouse must sacrifice its own capital, a layer known as “skin-in-the-game.” This operational penalty aligns incentives, forcing the exchange to maintain conservative margin standards during periods of peace.

If the loss breaks through the exchange’s capital defense, the waterfall reaches the mutualized default fund. The clearinghouse draws cash directly from the deposits of surviving clearing members—effectively sacrificing peripheral institutions to preserve the integrity of the core market.

WHY IT MATTERS NOW

High-frequency algorithmic trading and massive passive index flows concentrate systemic risk inside a few globally systemic clearinghouses, such as CME Group and ICE Clear. A failure at any of these nodes would instantly freeze trillions of dollars in global capital markets.

Regulators under frameworks like Dodd-Frank and EMIR mandated central clearing for over-the-counter derivatives to prevent another Lehman Brothers style bilateral collapse. This regulatory shift did not eliminate systemic credit risk; it merely concentrated it into a handful of centralized clearing nodes.

Modern volatility triggers are faster and more aggressive than those observed in historical crises. Rapid, concentrated options positions and algorithmic liquidations can generate multi-billion-dollar losses within seconds, testing the physical speed of the default waterfall.

In 2018, a single private energy trader in Europe defaulted on Nasdaq Clearing, instantly wiping out the entire default fund of the commodities unit. Surviving members had to inject over one hundred million euros within 48 hours to restore systemic balance, proving that default waterfalls are actively targeted by volatile market disruptions.

WHAT MOST PEOPLE MISS

Most financial observers believe that central clearinghouses possess infinite survival capital. They assume the clearinghouse exists to protect every individual member from taking losses.

In reality, the clearinghouse is a survival machine designed to protect the exchange, not its members. The default waterfall is a mathematical buffer system that systematically mutualizes ruinous losses across surviving competitors, forcing healthy firms to capitalize the failure of their bankrupt rivals to keep the centralized ledger open.

THE TRAJECTORY

Next 12–36 Months: Regulators will force clearinghouses to significantly expand their “skin-in-the-game” tranches. This prevents clearinghouses from immediately offloading early-stage defaults onto surviving clearing members, shifting the financial burden back onto exchange operators.

Next Five Years: Clearinghouses will automate the calculation and collection of intraday default fund contributions. Using real-time risk-modeling systems, the default waterfall will dynamically expand and contract based on continuous, millisecond-by-millisecond evaluations of active broker exposure.

Next Ten Years: Decentralized ledger networks will pilot atomic, smart-contract-driven clearing architectures. These networks will automatically liquidate positions at the moment of threshold breach, theoretically eliminating the need for multi-tiered default funds and manual mutualization cycles.

What Could Go Wrong: A simultaneous default of two or more tier-one clearing members during a massive interest rate shock would break the mutualized default fund entirely. The resulting cash demands would exceed the aggregate liquidity of the surviving banking sector, forcing governments to execute massive taxpayer-funded clearinghouse bailouts.

Most Likely Outcome: Clearinghouses will consolidate further, becoming de facto public utilities. Central bank liquidity lines will eventually backstop the bottom-most layers of the default waterfall, institutionalizing the ultimate reality that central clearinghouses are simply too systemic to fail.

KEY TERMS

- Default Waterfall: The sequential order of financial resources used by a central counterparty to absorb clearing member losses during a default.

- Skin-in-the-Game (SITG): The capital that a clearinghouse must contribute to the default waterfall before mutualizing losses among surviving clearing members.

- Loss Mutualization: The risk-sharing mechanism where surviving clearing members collectively absorb the losses of a defaulting member using pre-funded default pools.

- Initial Margin: The collateral deposited by a clearing member to cover potential future losses during the liquidation of their portfolio.

- Variation Margin: Daily or intraday cash payments made to reflect mark-to-market price changes, preventing the accumulation of uncollateralized risk.

SOURCES

- Committee on Payments and Market Infrastructures (CPMI) — Resilience of central counterparties (CCPs): Association and default water resources

- European Market Infrastructure Regulation (EMIR) — Technical Standards on Clearing Member Default Waterfalls

- CME Group — Financial Safeguards: Risk Management and the Default Waterfall

- Journal of Financial Market Infrastructures — Stress Testing and Loss Allocation in Central Counterparties